Uber Eats: SEO aggregation case study

Uber Eats: SEO aggregation case study

Uber Eats is a smart product expansion but also a smart SEO aggregator play. In this article, I explain how it works and why it might have saved Uber.

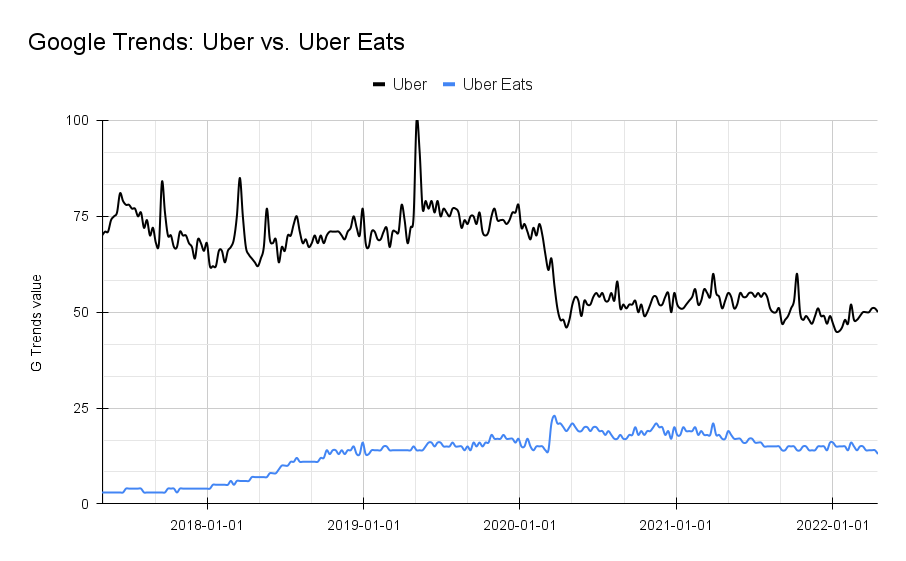

UBER is both, a winner and a loser of the Covid pandemic. Its ride hailing business came to a brutal stillstand in March 2020 and hasn’t fully recovered since. And yet, Uber became profitable in late 2021. Why? Because of Uber Eats.

Uber’s food delivery arm exploded at the same time its ride hailing business crashed. You can even see the flip in Google Trends:

Since 2021, Uber Eats drives more than 50% of total revenue. It’s a case study of a company that first didn’t have strong SEO leverage and then found a path to SEO scalability by expanding into an aggregation play.

Uber Eats, a logical product expansion

Before covering the SEO play, let’s talk about the product evolution.

Uber started as a marketplace that connects drivers with riders. Since it’s a realtime service, there is no inventory that UBER could expose to Google, address searches and drive organic traffic. Zillow has homes. Tripadvisor has Hotels. But Uber doesn’t have inventory that’s stable enough. Its value is defined by how long it takes to connect drivers with riders (shorter = better). They want to churn through Inventory as quickly as possible.

Expanding into food delivery was a smart play by Uber because the business dynamics are different but complementary. Drivers are already transporting people - why not food?

Uber Eats is a triple-sided marketplace (riders + eaters + restaurants) while Uber Core is a two-sided marketplace (riders + drivers). Restaurants is an inventory that’s stable enough for Uber Eats to expose in Google’s search results.

Uber Eats = aggregator

Aggregators can scale SEO much easier than integrators because of the way they create content. Aggregators use inventory (often user-generated) to drive search traffic, integrators have to create the content themselves. The product and market dictate the route.

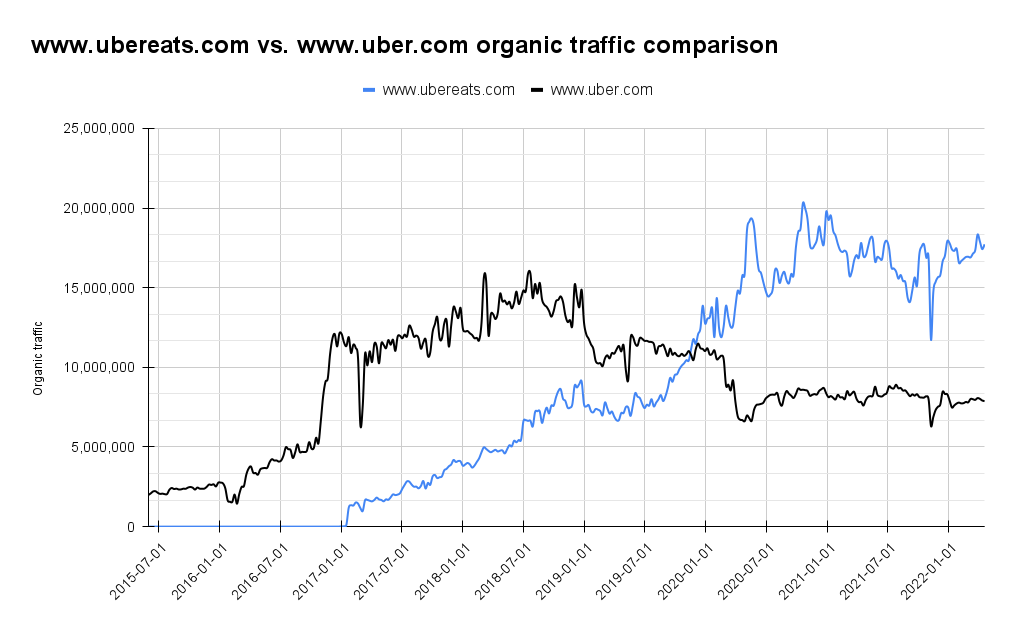

Ubereats.com surpassed uber.com in organic traffic when the pandemic broke out. Brand traffic to uber.com decreased when ride hailing crashed due to the Covid virus in March 2020. But another reason is the aggregator dynamic of Uber Eats.

Uber.com’s SEO strategy is very similar to that of integrators:

Heavy focus on content marketing

High degree of brand traffic

Focus on a few crucial head terms

Leverage is limited for the rider since users don’t search for a ride on Google; only potential drivers might. Uber.com does rank for competitive keywords like “taxi service near me” and has a pricing calculator for riders. It also ranks for keywords like “rent a tesla” on the driver side.

Ubereats.com gets over 8M monthly visits from organic search, compared to the 6.5M to uber.com. Over 60% of organic traffic to ubereats.com is non-branded, compared to almost 90% branded traffic to uber.com. That’s what the aggregator playbook is all about: you’re able to target a lot of non-branded keywords.

The best part: your number of pages scales with the business. The more restaurants Uber Eats partners with, the more keywords they can go after. Even for the popular “x near me” keywords that are so important for the business Uber has a higher chance to compete the more restaurants they can show in close proximity to people. The value of a “x near me” page grows with more restaurants. This is a dynamic unique to aggregators and the reason why expanding into this direction was a smart play by Uber.

Competing with the same inventory

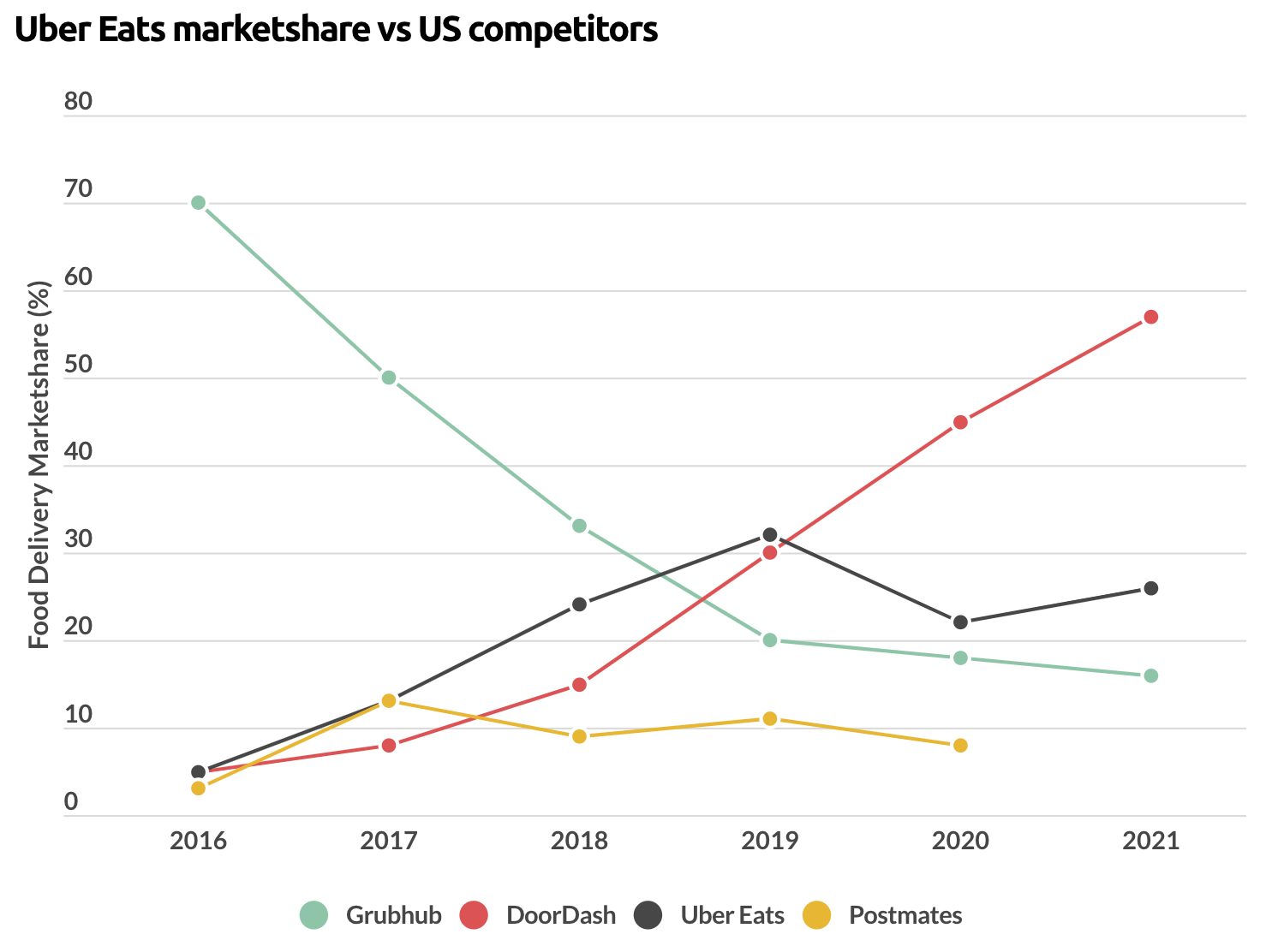

Expanding into other markets means competing with other companies. Uber was able to win the ride hailing market in terms of market share but not the food delivery market.

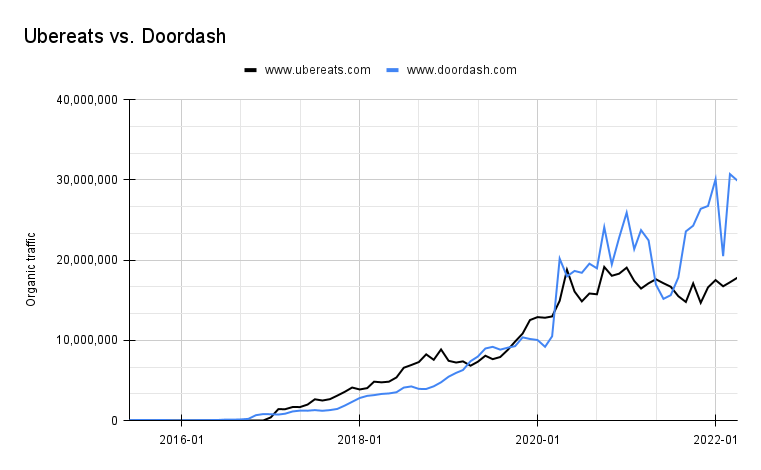

Doordash overtook UberEats in Organic Traffic in March/April 2020. Its organic traffic in April 2022 sits at roughly 21M monthly visitors from non-brand traffic, compared to Uber Eats’ 5M.

Few companies (Google, Amazon, Apple) can compete well in two markets. Uber is #1 in ride hailing and #2 in food delivery in the US. Even after buying Postmates, UberEats’s market share is much smaller than DoorDash’s.

As both companies have an increasingly similar inventory, the way they leverage it to compete with each other is interesting. Take these two pages that one of the most important keywords in the space “chinese food near me” (4.1M monthly searches):

https://www.doordash.com/cuisine/chinese-near-me/ (ranks #1)

https://www.ubereats.com/near-me/chinese (ranks #4)

Doordash has different city sections on the page (apparently sorted by city size), FAQ at the bottom. Uber Eats shows a large selection of restaurants, including their delivery fees and approximate delivery times. Uber also has FAQ at the bottom of the page and is the only site in the top 10 with an FAQ snippet.

All these details (title structure, onpage content, information depth, relevance of results, etc.) matter at this scale. Note that Doordash’s page has the fewest backlinks of all top results. The importance of backlinks is another common difference between aggregators and integrators. Aggregators need to focus on internal linking, integrators more on backlinks.

After all, UberEats is still a success story. Uber, the whole company, just became (EBITDA) profitable and it’s because of Uber Eats. Companies that can expand into aggregator territory should take note. [1]